You’ve heard the term “blockchain” a lot lately, haven’t you? It often comes up when discussing Bitcoin, new technologies, or the digital future.

It’s not surprising if you find it difficult, complex, or highly technical to understand. But did you know that its basic idea is very simple and anyone can grasp it?

So, what is blockchain? And why is everyone talking about it?

This guide will take you step-by-step through what you need to know as a beginner, in a very easy and clear way, far from technical complexities.

What is Blockchain? Let’s Start with the Simplest Analogy

It’s a shared, secure digital ledger where all transactions and data are recorded in a way that makes it extremely difficult to change or tamper with after they’ve been registered.

Imagine you have a private notebook. Now, imagine this notebook has been copied thousands of times, and these copies are distributed to thousands of people around the world.

When you or anyone else wants to add new information (a new page), a majority of these people must verify the information and approve it. Once approved and the page is added, absolutely no one can change what was written on it.

This is the fundamental idea of blockchain: it is a digital notebook, a special and advanced type of database used to record information (like financial transactions, contracts, or any other data) in a very secure, transparent to everyone, and immutable (unchangeable) or tamper-proof way.

What are the Components of a Blockchain?

To better understand how blockchain works, let’s first get acquainted with the blockchain components, the basic parts that make up this digital notebook:

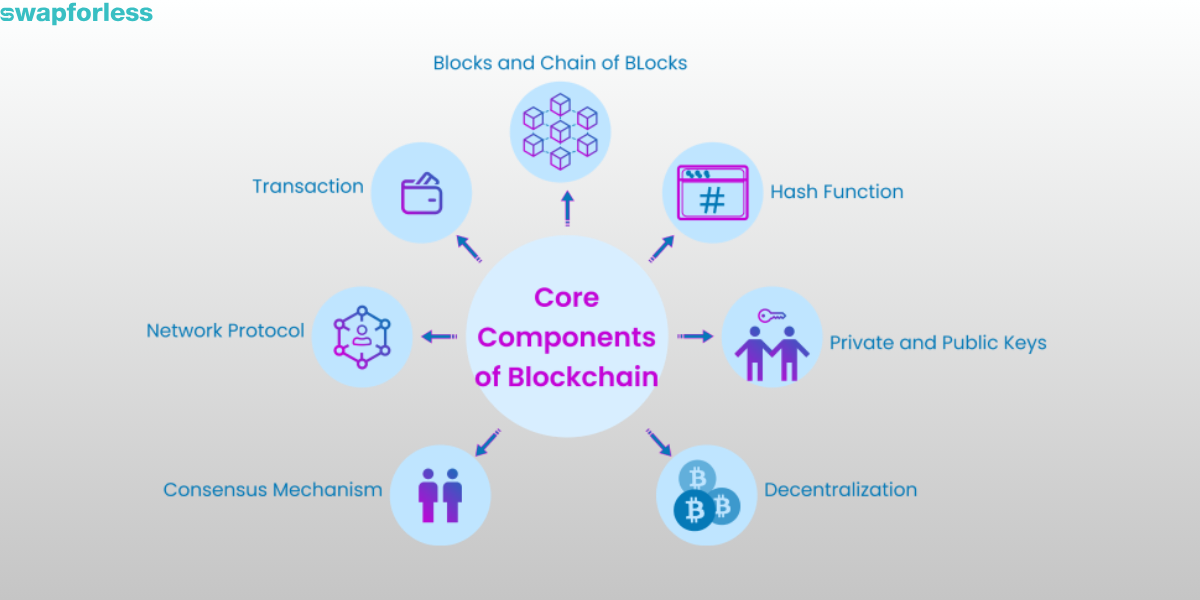

- Transaction: This is the piece of information you want to record in the notebook we talked about. For example, if you want to send an amount to someone else, recording this action is a “transaction.”

- Block: This is the “page” in the notebook. When a group of new transactions accumulates, they are bundled together into a single “block” to be recorded.

- Hash: Think of this as a unique “digital seal” or “digital fingerprint” for each page (block). This seal changes completely if even a single character on the page is altered, and it also contains the fingerprint of the previous page to link them together.

- Chain: When a new block is sealed, it’s linked to the block before it using this digital seal. This linking creates a connected “chain” of blocks, hence the name “block-chain.”

- Node: This is any person (or more accurately, a computer) that keeps a full, up-to-date copy of the notebook (blockchain) and participates in verifying new transactions and adding them.

- Distributed Ledger: This is the core concept that distinguishes blockchain. It means the ledger isn’t stored in one central place (like a central bank’s server) but is copied and spread across thousands of nodes around the world.

How Does Blockchain Actually Work?

Now that we know the blockchain components, let’s see how blockchain works when a new transaction is recorded:

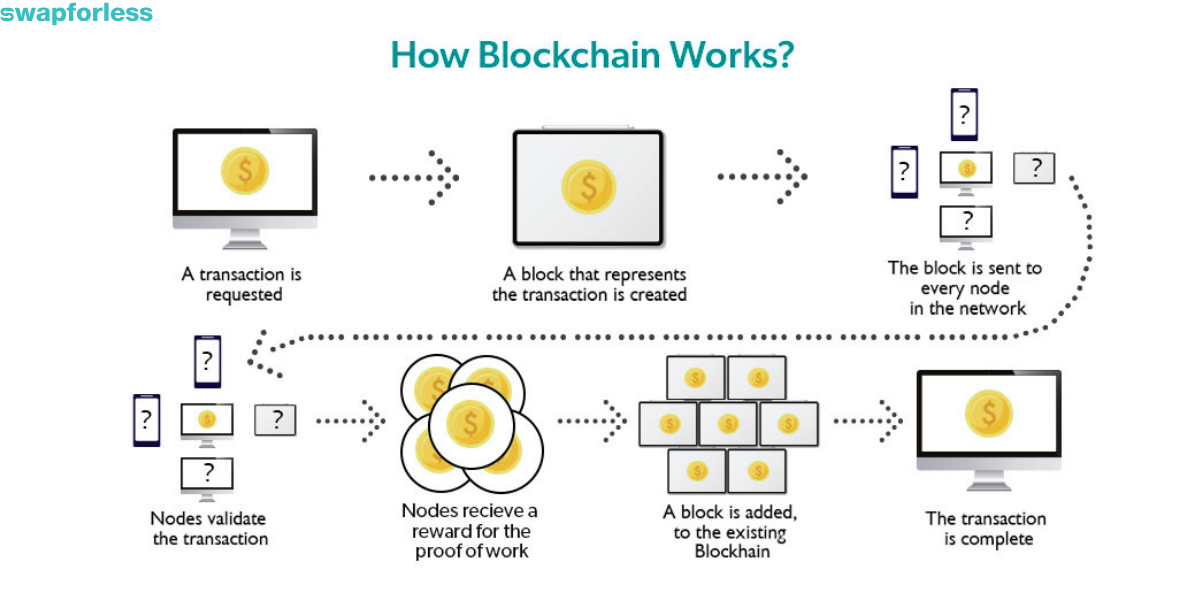

- A Transaction Occurs: Let’s assume you send a digital value to someone.

- Broadcast and Verification: Details of this transaction (encrypted and secure) are broadcast to all participating nodes (computers) in the blockchain network.

- Validation: The nodes verify the transaction’s validity based on agreed-upon rules (e.g., Do you actually own the amount you’re trying to send? Is the digital signature valid?).

- Block Formation: Validated transactions are bundled together with other transactions into a new “block” (page).

- Consensus: This is a crucial step. A majority of the nodes must agree that this new block is valid and acceptable. This agreement is reached using specific rules called a Consensus Protocol. Read What Are Consensus Mechanisms?

- Hashing and Linking: Once consensus is reached, the new block is “sealed” with its unique digital fingerprint (the hash) and linked to the last block in the chain.

- Update for Everyone: The new, sealed block is added to the copy of the ledger (blockchain) held by all participants. Your transaction is now a permanent, verified, and unchangeable part of the chain.

Are All Blockchains the Same? Types of Blockchain Networks

Not all blockchain networks are open to everyone in the same way. There are different types of blockchain networks based on access levels and control:

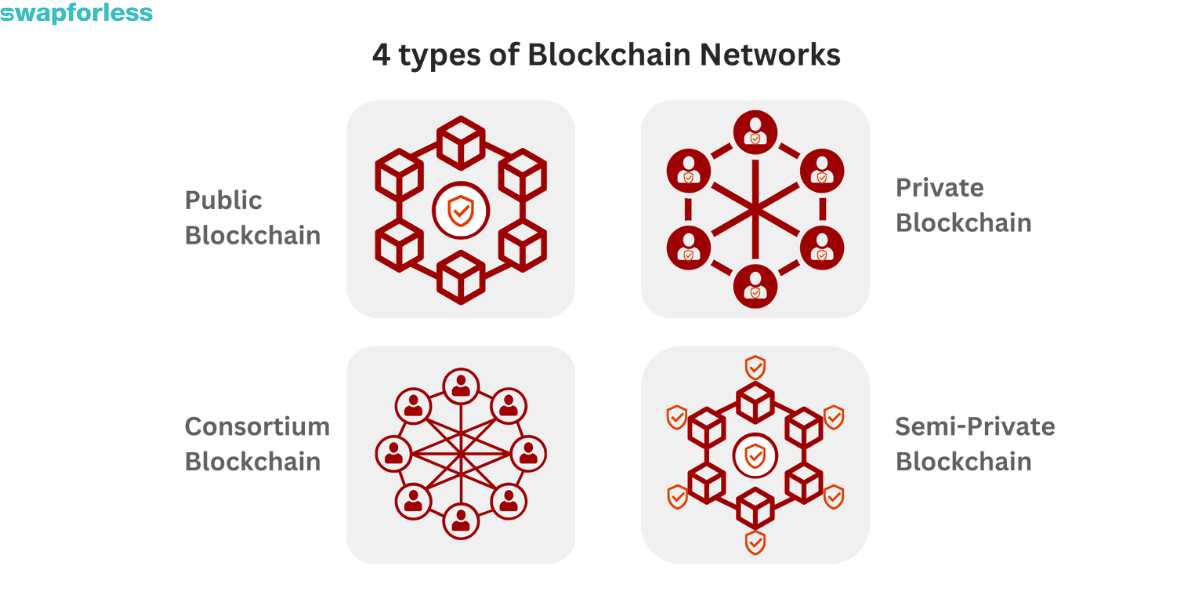

- Public Blockchain: Like the public internet. Anyone can join the network, view transactions (often pseudonymously), and participate in the verification process. They are highly decentralized (e.g., Bitcoin, Ethereum networks).

- Private Blockchain: Like a company’s internal network. Access requires permission and authorization, and it’s typically controlled by a single entity.

- Consortium Blockchain: Managed by a specific group of organizations, allowing them shared authority to manage the network.

- Hybrid Blockchain: Combines features of both public and private networks, allowing controlled access to sensitive data while maintaining some level of transparency.

Read more about What Are the Types of Blockchain Networks?

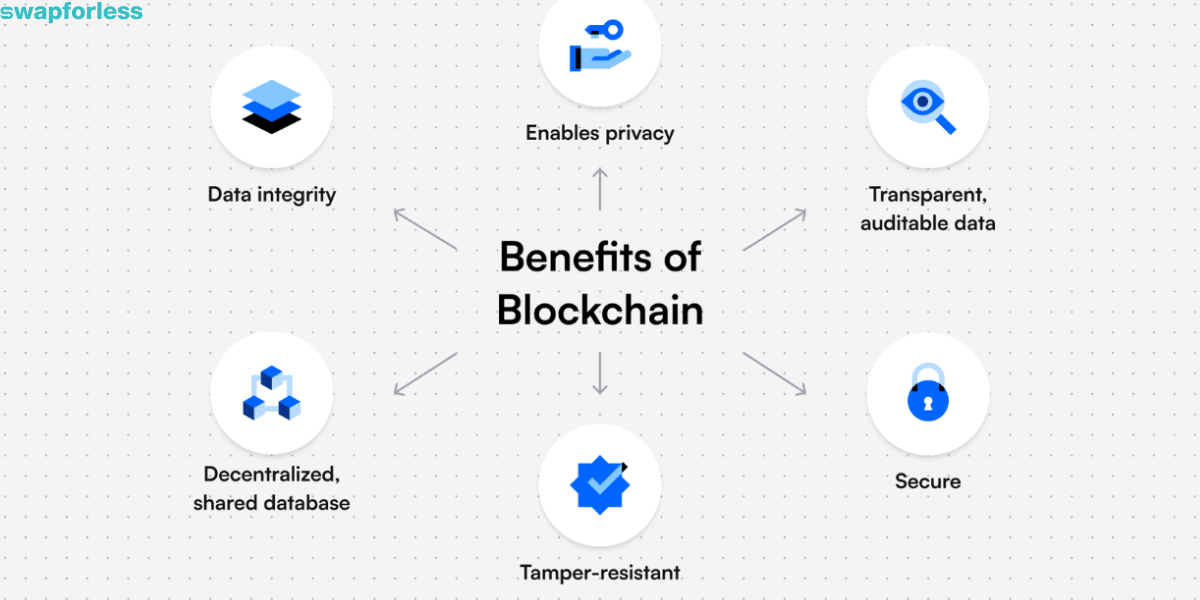

What are the Main Benefits of Blockchain?

Now you might wonder, what makes this technology special? What are the benefits of blockchain? Here are the most important ones:

- Decentralization: Data and transactions are distributed across a network of computers (nodes) instead of a single central authority, which increases system reliability and reduces the risks of failure or attacks. Read What is Decentralization?

- Transparency: Because the ledger is distributed and accessible, authorized parties can easily verify information, increasing trust and reducing the need for intermediaries.

- Security: Due to its distributed nature and strong cryptography, blockchain is highly resistant to hacking and data tampering. There is no single point of failure to target.

- Immutability: Once a transaction is recorded in a block and added to the chain, it’s practically impossible to change or delete it without the consensus of the entire network (which is extremely difficult).

- Efficiency and Cost Reduction: Many traditional processes involve numerous intermediaries that slow things down and add costs. Blockchain can eliminate the need for some intermediaries, making processes faster and cheaper.

Does Blockchain Have Drawbacks or Challenges?

To be fair, despite all the advantages, blockchain technology still faces some challenges and drawbacks that are being worked on:

- Speed and Scalability: Some blockchain networks, especially older ones like Bitcoin, can only process a limited number of transactions per second (around 10 TPS for Bitcoin, for example). This is very slow compared to traditional payment systems like Visa.

- Energy Consumption: Some types of blockchain that rely on a consensus mechanism called “Proof-of-Work” (PoW), most famously Bitcoin, require enormous amounts of electrical energy to secure the network and validate transactions.

- Potential for Illegal Use: Although transparency is a feature, the degree of privacy and difficulty in tracing real-world identities on some networks might make them attractive for illicit activities.

- Data Storage: Since blockchain permanently records every transaction, its size grows continuously over time. This growth can pose challenges in terms of cost and physical space required for storage in the long run.

- Regulation and Laws: Governments and regulatory bodies worldwide are still working on establishing clear laws and regulations for its various uses.

- Complexity: Despite simplification efforts, some aspects of using or understanding blockchain technology still require a certain technical knowledge, which can be a barrier for the average user.

Is Blockchain Secure, as Claimed?

Generally speaking, yes. The fundamental design of blockchain technology provides a very high level of security. Is blockchain secure? The answer lies in these reasons:

- Decentralization: No single person or entity can control or shut down the network. Attacking it would require controlling a vast number of devices simultaneously.

- Cryptography: The use of hashes (seals) makes falsifying transactions or altering past blocks computationally almost impossible.

But be aware: The security of the blockchain “network” itself doesn’t mean everything related to it is 100% secure. Weaknesses can appear in:

- Applications built on top of the blockchain (DApps): These might contain software bugs that can be exploited.

- Digital Wallets: If you don’t keep your private keys safe, you could be robbed.

- Centralized Platforms: Cryptocurrency exchanges can be hacked.

Security depends on the strength of the network itself plus how you use the applications associated with it.

Is Blockchain the Same as Bitcoin?

This is one of the most common misconceptions. The answer is no.

- Blockchain is the technology; it’s the underlying infrastructure (think of it like the internet).

- Bitcoin is the first successful application built using blockchain technology to create a decentralized digital cash system (like the first major website on the internet).

Blockchain technology can be used to build thousands of different applications, many unrelated to money, just as the internet can be used for many things beyond browsing websites.

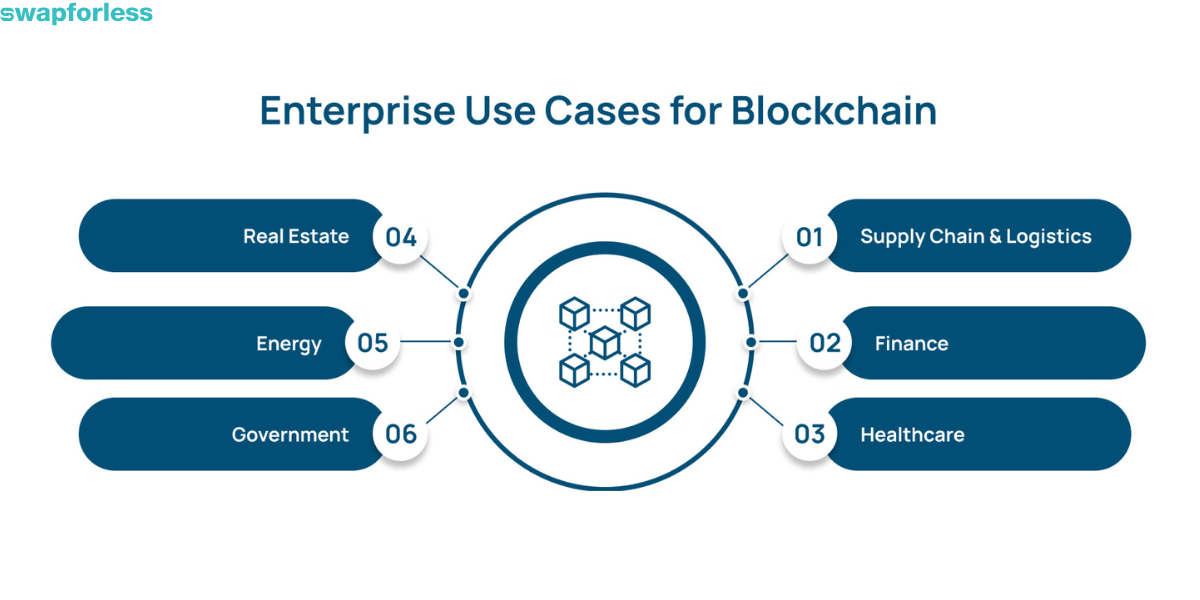

What are Other Interesting Use Cases for Blockchain?

Now that you know blockchain isn’t just for cryptocurrencies, what are the other blockchain use cases? The possibilities are vast and growing:

- Supply Chain Tracking: Tracking products and goods (like food, medicine, luxury items) from producer to final consumer step-by-step, verifying quality and authenticity.

- Property Records: Creating secure, transparent, and tamper-proof ownership records for real estate and other valuable assets, simplifying buying/selling and proving ownership definitively.

- Banking and Finance: Significantly speeding up international transfers, reducing their costs, facilitating lending, increasing transparency in financial transactions, and reducing fraud.

- Cryptocurrencies: The most famous use case, where blockchain provides a secure and decentralized ledger for transactions (e.g., Bitcoin, Ethereum).

- Electronic Voting: Designing voting systems where each vote is recorded securely and immutably while maintaining voter anonymity.

- Medical Records Management: Storing medical histories securely and encrypted, giving patients control over who can access their information.

- Smart Contracts: Small programs running on the blockchain that automatically execute the terms of an agreement when certain conditions are met.

Want to know more details about Smart Contracts? Read What Are Smart Contracts? A Practical Guide in 2025

In Conclusion

So, what is blockchain? Simply put, it’s an ingenious way to record and share information securely, transparently, and reliably among a large group of people without needing a central intermediary.

It might seem technical at first, but understanding the basics of blockchain opens the door to grasping many of the digital advancements happening now and shaping our future.